On August 28th, several policy announcements related to individual income tax were released by the Ministry of Finance and the State Taxation Administration of China. These policies aim to provide relief to taxpayers and support various aspects of taxation to stimulate consumption and investment.

To help you understand the what was presented in the announcement, our team has created a summary of each policy.

1) Annual One-time Bonus Individual Income Tax Policy

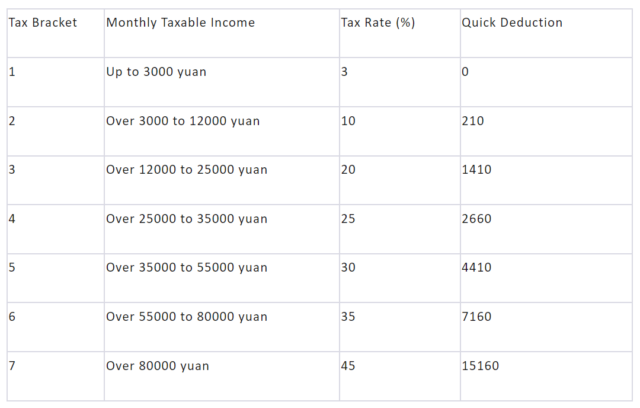

Consolidated income tax rate table based on monthly conversion

2) Individual Income Tax Policy for Foreign Individuals Regarding Allowances and Subsidies

3) Policy on Comprehensive Income Settlement and Payment for Individual Income Tax

-

-

-

-

-

Their annual comprehensive income does not exceed 120,000 yuan, and they are required to settle and pay supplementary tax, or -

The amount of supplementary tax to be settled and paid does not exceed 400 yuan.

-

-

-

-

4) Individual Income Tax Policy for Personal Income from Listed Company Equity Incentives

Resident individuals who acquire stock options, stock appreciation rights, restricted stock, and other equity incentives (hereafter referred to as equity incentives) that meet the conditions specified in several official notifications (dated 2005, 2009, 2015, and 2016) will not have these incentives incorporated into their annual comprehensive income. Instead, they’ll be taxed separately using the comprehensive income tax rate table.

The tax calculation is:

Tax payable = Equity incentive income × Applicable tax rate – Quick deduction.

If an individual taxpayer receives stock incentives two or more times (including twice) within a tax year, the incentives should be combined for tax calculation.

5) Individual Income Tax Policy for Personal Partners of Entrepreneurial Investment Enterprises

The notice from China’s Ministry of Finance, the State Taxation Administration, the National Development and Reform Commission, and the China Securities Regulatory Commission primarily focuses on the procedures Chinese venture capital firms should follow when calculating personal income tax for their partners.

Venture capital firms can opt for one of two methods to determine personal income tax: they can either base calculations on a single investment fund or compute based on the firm’s annual total income. For those choosing the single investment fund method, income derived from the transfer of equity and dividends is taxed at a 20% rate. In contrast, if they opt for the total annual income approach, the income is taxed progressively at rates ranging from 5% to 35% depending on the amount.

Several detailed provisions are provided for calculating tax using the single investment fund approach, including how to account for income from equity transfers and dividend receipts. Certain expenditures, like the fees and remunerations for the fund managers, cannot be deducted in these calculations.

If venture capital firms decide on the total annual income method, it involves summing up the year’s total income, subtracting costs, expenses, and losses, and then determining the amount to be distributed to individual partners. Special provisions allow for certain deductions under specified conditions.

Once a venture capital firm selects a method, they are bound to it for three years. They must also register their chosen method with the relevant tax authorities.

6) Notice on the Continuation of Individual Income Tax Preferential Policy for the Guangdong-Hong Kong-Macao Greater Bay Area

Disclaimer: The information contained in this article is for general informational purposes only and should not be construed as legal, tax, financial, or professional advice. The content is based on current facts, circumstances, and assumptions, and its accuracy may be affected by changes in laws, regulations, or market conditions. While we strive to ensure the accuracy and completeness of the content, Azure Group China and any associated Azure Group entities, member or employee, disclaim any liability for any loss or damage incurred by individuals or entities relying on the information provided herein, whether arising from negligence, errors, omissions, or any other cause. Readers are advised to consult with qualified professionals for advice specific to their situation before taking any action.